Fed Rate Cut Guidance Will Exceed Wall Street’s Bearish Outlook

Publikováno: 17.12.2024

The cost of borrowing money will likely continue to drop, underpinning riskier assets like bitcoin, says Scott Garliss.

Wall Street’s rate cut outlook is overly pessimistic.

This week brings an important update for investors everywhere. The Federal Reserve will update its interest rate policy on Wednesday Dec. 18. The consensus expectation is for a 25 basis point cut, lowering the effective rate to 4.4% from the current level of 4.7%.

The more important part of the discussion will be the outlook for the path of interest rates next year. Investors want to know whether policymakers still intend to lower rates by another 100 basis points next year, as the group endorsed in September, or if the viewpoint has grown more hawkish (i.e. less inclined to ease).

Back in September, Wall Street was certain those four rate cuts would happen by the end of 2025. But today, money managers and traders aren’t quite so certain. According to the Chicago Mercantile Exchange’s FedWatch tool, bond-market speculators are betting our central bank will lower interest rates by just 50 basis points next year.

I agree with some of that assessment. The Fed is likely to reduce interest-rate expectations for next year. Recent employment and inflation numbers show the pace of growth is returning to pre-pandemic levels of normal. At the same time, economic output hasn’t collapsed like some of the dire predictions earlier this year. That tells me the Federal Reserve is achieving its goals of full employment and price stability. Consequently, I think it will guide for 75 basis points worth of rate cuts in 2025 versus Wall Street’s outlook for just 50.

This is important for us as risk-asset investors because it means the cost of borrowing money will continue to drop. As the access to funds gets cheaper, more people will take out loans. Hedge funds will lever up. There will be more money available in the financial system to invest. At the same time, the payout for money market funds and bonds will decline because interest rates are falling. That means investors will seek out better returns in risk assets like cryptocurrencies and stocks, driving those prices even higher.

But don’t take my word for it, let’s look at what the data’s telling us.

For anyone unfamiliar, the Fed meets to set policy just eight times a year. Typically, those gatherings happen in the first and last month of each quarter. The second meeting of each quarter takes on an added significance. Those are the meetings when we receive policymakers’ Summary of Economic Projections (“SEP”).

At those meetings, each member of the Board of Governors and the regional Fed banks are asked to project where they see economic growth, inflation, unemployment, and interest rates heading over the coming years. The data is then compiled to find the median outlook for each of those categories. Those results don’t guarantee monetary policy will follow the same course, but they give us an idea of its direction.

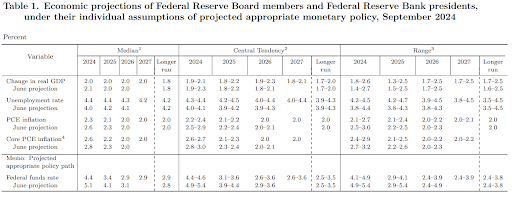

Here's what the September SEP forecast looked like:

The part of the tables we care about most are the median projections on the left. By surveying those numbers, we get an idea of policymakers’ outlook for growth, inflation, unemployment, and interest rates for this year through 2027. As you can see, Fed officials predicted gross domestic product (“GDP”) growth ending this year around 2%, an unemployment rate of 4.4%, inflation at 2.3%, and borrowing costs at 4.4%. Then, in the out years, the group expects each measure to stabilize, with interest rates settling at 2.9%.

We’re unlikely to end this year in line with those September projections. Based on economists’ expectations, GDP will increase 2.2% in the fourth quarter. That would put the average rate of economic growth this year at about 2.4% – above the prior expectation.

And it’s a similar story for the other metrics. According to the November labor data, the unemployment rate sits at 4.2% while October personal consumption expenditures showed inflation growth is at 2.3% compared to a year ago. Those metrics are roughly in line with the prior expectations, supporting a 25 basis point rate cut this week.

But the rate-cut outlook will be decided by the employment and inflation trends, and both of those are headed in the right direction.

First, let’s observe the pace of nonfarm payroll gains. According to the November numbers, the economy has added an average of 180,000 jobs per month in 2024 compared to the 177,300 average from 2017-2019. That tells policymakers the labor market is stabilizing after years of hyper growth, and returning to normal.

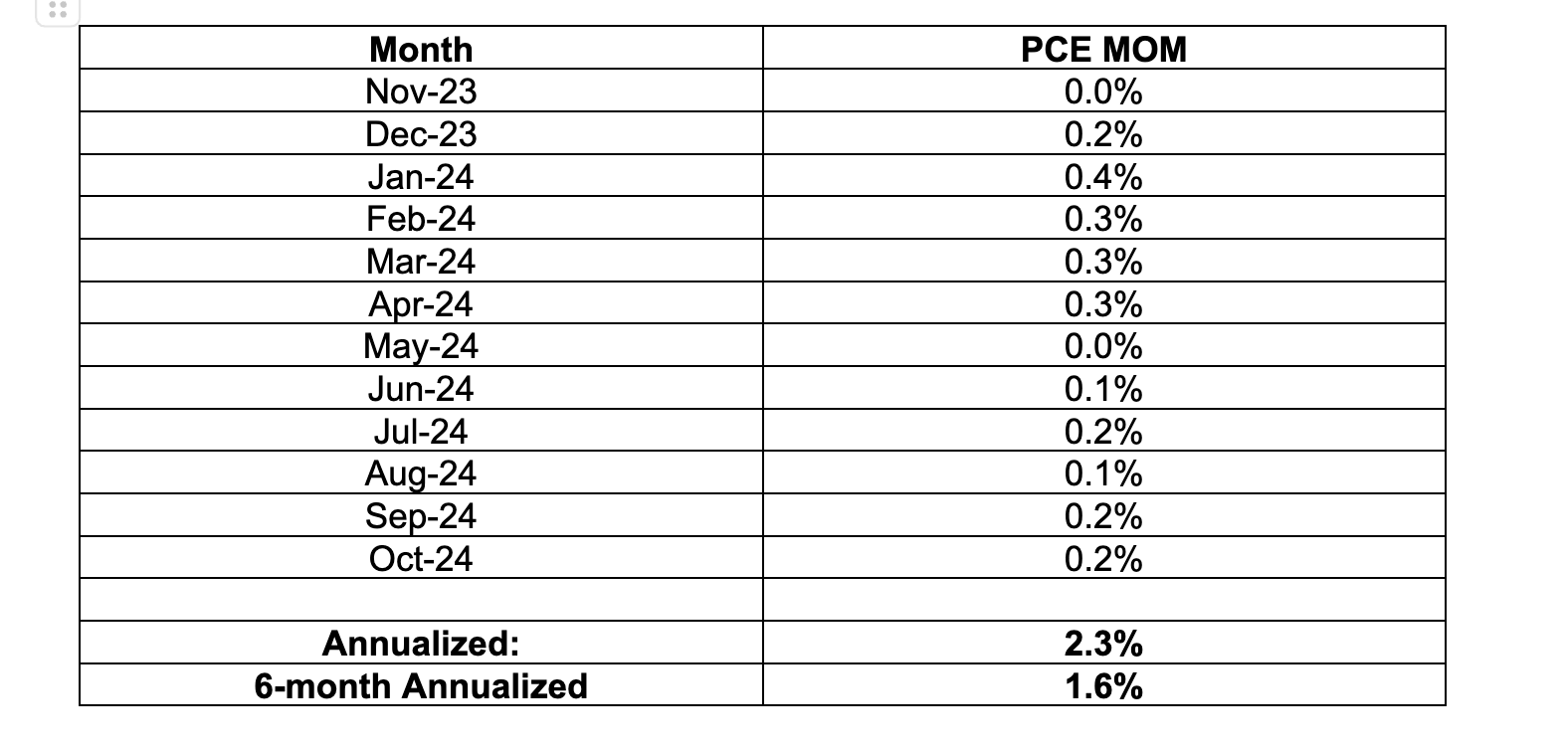

The story isn’t much different with inflation. Take a look at the trend in personal consumption expenditures:

The above table shows us PCE growth by month over the last year. As I’ve been highlighting, price pressures appear hotter than anticipated due to high numbers from the start of this year. January through April account for 1.3% of November’s 2.3% annualized result. But, if we look at the past six months, we see the forward-looking pace shows annualized inflation growth has slowed to 1.6%. That’s well below the Fed’s 2% target and signals interest rates are still weighing on prices.

Since the Fed started raising rates in March 2022, it’s had two goals in mind: maximum employment and stable prices. Until recently, it hasn’t seen concrete signs of either scenario playing out. But, based on the numbers we just looked at, policymakers now have evidence that the labor market has steadied, and price pressures are coming back to target.

From 2000 to 2020, the real rate of interest based on PCE (effective fed funds minus inflation) has had an average rate of -0.05%. Currently, the rate sits at 2.6%. If our central bank is trying to get that number back to neutral (neither hurts nor helps the economy), a lot of easing lies ahead.

At the end of the day, the economy is still doing well. As a result, the Fed doesn’t have to be as aggressive with its guidance for rate cuts moving forward. In fact, this is exactly what it wants: economic growth that’s holding up and affords it the ability to take its time. We don’t want a central bank cutting rates rapidly because output is in a free fall.

So, like I said at the start, expect the Fed to endorse borrowing costs ending 2025 around 3.7% compared to the prior guidance for 3.4%. That will be lower than Wall Street’s current expectation for 3.9%, easing worst-case fears. And the change should support a steady, long-term rally in risk assets like bitcoin and ether.