Does Apple's 15% platform cut change the game?

Publikováno: 23.11.2020

And why did they do it?

[The GameDiscoverCo game discovery newsletter is written by ‘how people find your game’ expert & GameDiscoverCo founder Simon Carless, and is a regular look at how people discover and buy video games in the 2020s.]

We’re back, and firstly, thank you so much to everyone who subscribed to the new GameDiscoverCo Plus paid data/newsletter tier that we announced last week. (We already got a nice ‘milestone’ email from Substack about the number of subscribers.)

Anyhow, your support helps make this newsletter possible! The next Plus-exclusive newsletters (weekly Steam Hype charts, and that stat-filled Apple Arcade platform overview) are going out over the next few days to paid subscribers. But in the meantime… it’s regular newsletter time!

Apple’s platform cut - reactions and ramifications

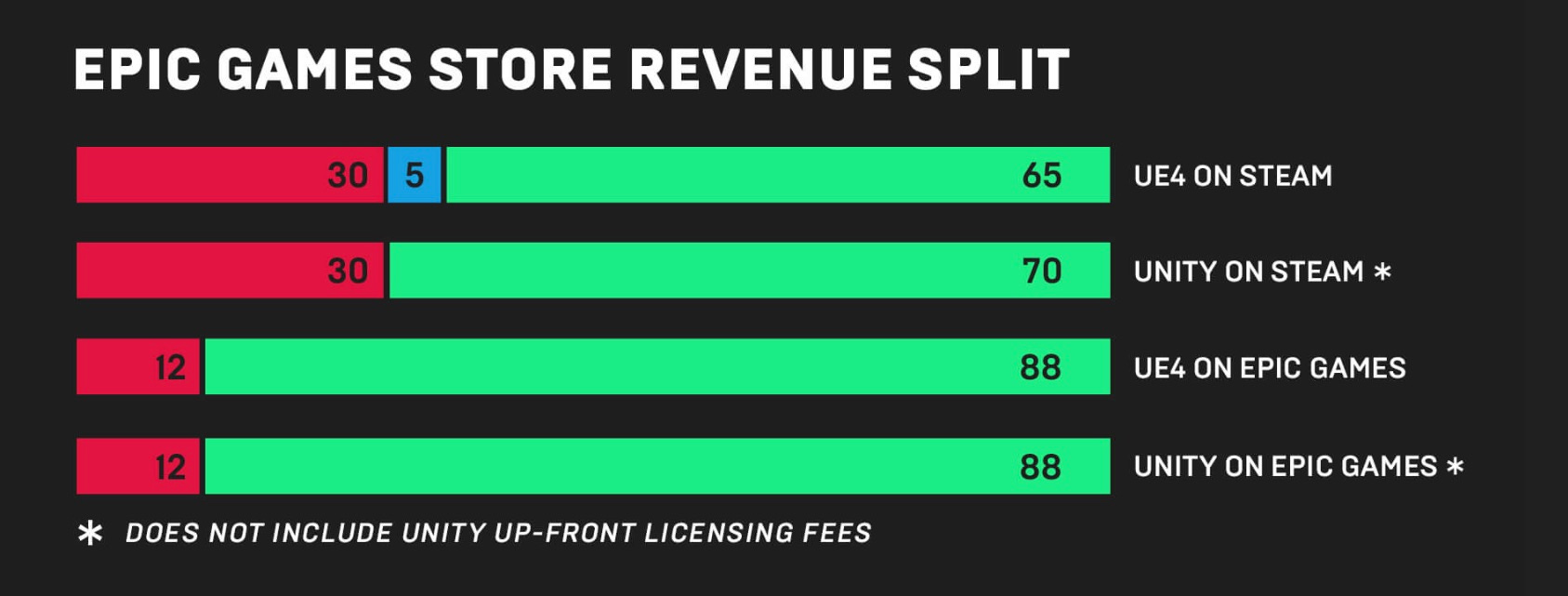

So as you doubtless heard, Apple has announced the App Store Small Business Program, a major and permanent change to the flat 30% platform cut for apps and games on iOS (and I presume the Mac) App Stores.

The change “reduces App Store commission to 15 percent for small businesses earning up to $1 million per year”, starting in January 2021. So that means that all game devs earning $1mil or less per year across all of its apps (after Apple’s cut) get an extra 21.4% revenue.

Now obviously, the vast majority of revenue on iOS is from large-grossing free to play games or subscription apps. This Reuters piece has an estimate (though it’s on $1mil gross, not $1mil after Apple cut): “Sensor Tower said 97.5% of iOS developers generated less than $1 million per year in gross consumer spending. But those same developers contributed only 4.9% of the App Store’s 2019 revenue.”

So, this affects a lot of developers - which is great, although I don’t really know many game devs who make a regular living in this kind of revenue range on Apple. (I definitely do on Steam!) But it doesn’t affect Apple’s major app/game partners.

This is interesting, because you’d think Apple would want to keep a good relationship with its biggest partners. And this hints at the real issue. Apple’s big customers - yes, including Epic - are already mad at them, and trying to get European and U.S. government to act on antitrust concerns. (Or in Epic’s case, outright suing them.)

So I definitely read the move - though generous in the abstract - as Apple’s window dressing for any possible government suits in the future. And indeed the Apple PR re-iterates its bottom line: “The App Store’s standard commission rate of 30 percent remains in place for apps selling digital goods and services and making more than $1 million in proceeds… earlier this year, an independent study by the Analysis Group found that Apple’s commission structure is in the mainstream for app distribution and gaming platforms.”

But how about Steam, Sony, Microsoft & revenue cut?

What does this mean for other platforms? Well, Valve already made a call with Steam back in November 2018, and that call was the opposite: “For all sales between $10 million and $50 million [of a single game on Steam], the split goes to 25 percent. And for every sale after the initial $50 million, Steam will take just a 20 percent cut.” Valve cites the ‘network effect’ of large games bringing more users to Steam.

In typical Valve form, this is spot-on and true from a engineer-led logic point of view, but not super good PR for small devs - and is ultimately a ‘rich get richer’ move. Though actually it’s true that major publishers like EA, Microsoft and Sony have only been adding titles to Steam recently. And I think Sony and Guerrilla’s Horizon Zero Dawn: Complete Edition might already be in the 20% cut revenue range already.

Of course, Epic sees 12 percent as the correct platform cut (see above). But I don’t really buy the ‘reverse engineering costs’ approach as the ultimate arbiter of price for a for-profit company that can charge what it wants. Even Mr. Sweeney and friends aren’t doing that for - for example - the cost vs. revenue of making a Fortnite skin, right?

And - unlike iOS - I don’t think you can easily argue to government regulators that Steam is an unfair monopoly on an open PC video game platform, given that players can pick any store they want. Heck, companies like Epic are already using price differentiation to compete with them.

(BTW, I found this editorial on Apple’s ‘15% deflection tactic’ interesting. I may agree that mobile and AR/VR devices should also have complete choice of store and payment platform. But I’m not sure that this choice on the PC has led to a massively different $ experience for small or medium-sized game devs. Though it does allow large companies to distribute independently.)

As for Sony and Microsoft - or Nintendo? Because they have clear competitors - and are actually moving into other platforms for streaming purposes - I don’t see many calls to change their 30% cut. (Perhaps a limited set of devs being approved for the platform also creates a tension, and means that creators are reluctant to push back?)

The bottom line?

I think this is ultimately a problem of capitalism. It goes like this:

- company gets there first and maybe even does a good job

- takes market share for their platform and generates excess profits

- is a company and so answers to its shareholders and not its community of developers

- so discussions of ‘developer fairness’ directly clash with the profit motive

(This was also a problem at companies I’ve previously worked at.)

There’s no easy fix. Personally, I’d like to see more solutions like investing company The Vanguard Group (created by index fund pioneer John Bogle), which essentially is owned by the people who invest in it. So there’s no external shareholders with different motives. Many traditional financial investment companies charge 1% or more in yearly fees for their index funds, and Vanguard often costs less than 0.1%.

How this would work in games? Well, you’d need to have a company that:

- had a very large market share as a platform

- and then was willing to switch to a model where it gave shares to all of its developers, based on their sales

- and then let the developers control the company’s strategy and fees as shareholders. (A non-profit model could also work, but they can tend towards the disorganized over time.)

This whole concept is, well, probably a tall order. Right now on PC, the most egalitarian platform, Itch.io, has a pretty small market share, as I discussed in a recent newsletter. So you can have the right intentions, but not have the share to make a difference. But I think it’s good to have a dream target model, right?

(A final caveat: most of the time when your game doesn’t make as much money as you wanted, it’s not an additional 21.4% revenue that’s the difference between making it or not. It’s generally a wider supply/demand issue for your game - not enough players, for whatever reason. Important to not conflate that with issues around % cut.)

The game discovery news round-up..

We’re going into Thanksgiving week here in there U.S., so you’d think it would be a quieter time. (Hope everyone is social distancing and keeping to social small circles, as you should!)

But no, there’s plenty going on - on all fronts. And here’s a giant round-up of some of the things you should care about on platform and discoverability that you might have missed:

Two notable upcoming Steam things: firstly, you can submit your unreleased game’s demo for the February 2021 Steam Game Festival until December 2nd. I highly recommend you do - short, sharp Festival demo appearances that may get picked up by streamers are the best demo appearances! And second, Fellow Traveller’s narrative games fest LudoNarraCon is back on Steam April 23rd-26th, 2021, and you can sign up if interested on their official website.

Following GameDiscoverCo’s survey of Week 1: Year 1 Steam $ sales, Kyle Kukshtel made an interactive webpage which lets you plugin your launch wishlists/cost - or gross Week 1 Steam revenue - and get possible gross Steam revenues up to Year 5. (Lots of caveats: use worldwide average price if putting cost in, your wishlists may convert worse, it’s all a giant crapshoot, etc. But it’s a fun indicative thought experiment.)

The performance of Microids/PlayMagic’s remake of early 2000s FPS XIII (itself based on a Belgian comic book) has been, well, remarkably terrible. And ICO’s Thomas Bidaux did some research and, ouch: “There are a grand total of 7 games currently available on Steam that are Overwhelmingly Negative. XIII is the only one under 10% of positive reviews. It is also the first game in that range released since 2017.” (The dev team ended up blaming the pandemic, but the game was as high as #2 in the GameDiscoverCo Steam Hype weekly charts when it released, so looks like a big expectations mismatch as well.)

That ‘medium/larger publishers Katamari-ing up smaller devs’ consolidation trend is continuing. Besides Microsoft’s buying spree of late, some indie publishers are still doing it - Devolver buying Croteam after working with them for so long, Curve buying the For The King dev, and then of course, there’s Embracer Group, who picked up 13 studios the other day (lol!), including pinball dons Zen Studio and Flying Wild Hog. A trend to watch…

Seems like the PlayStation 5’s Store UI roll-out has still been a little rocky. For example, there was no ‘Deals’ section on PS5 (until a Black Friday-only section got added, but that’s more like a one-off section, one presumes?) Comments on the article are not a fan of the web PS Store, either: “The new store is slow to load on pc (using chrome), and I still don't see wishlist on the store… Must say that digging thru deals (or whole store at all) on mobile is one huge mess. Nameless repeating icons or microtext on them.”

Cloud gaming news: everyone is taking the webpage approach to iOS cloud game distro now, of course, with Nvidia’s GeForce Now debuting via Safari - and “Nvidia and Epic Games said Fortnite is also coming soon to Safari for iOS, with touch controls.” Huh! And on the Google front: “…it will begin public testing of its Stadia game service via the iOS Web browser within the next several weeks. ‘This will be the first phase of our iOS progressive web application,’ the company said.” We’ll see what user adoption is like via this slightly fiddly method.

Going deeper on Stadia, really dug this overview from The Verge of the cloud platform’s first year and prospects for the future: “Assassin’s Creed Valhalla and the hotly anticipated Cyberpunk 2077, which releases on December 10th, [are] crucial moments for Stadia. These releases… will define Stadia in the coming months, and [Google’s John] Justice knows it’s imperative Google treat CD Projekt Red’s big holiday launch as a make-or-break moment for the platform.”

Microlinks: congrats to The Game Awards nominees, a great range of games; interesting to check the Top 20 Epic Games Store games and see lotsa PS5 launch titles in there (Godfall doing great despite so-so reviews, Bugsnax, The Pathless); Superdata now trying to cover subscription service revenues: “Combined revenue [from Xbox Game Pass, PlayStation Now and EA Play] in October was up 142% year-over-year and subscriber numbers rose 113%.”

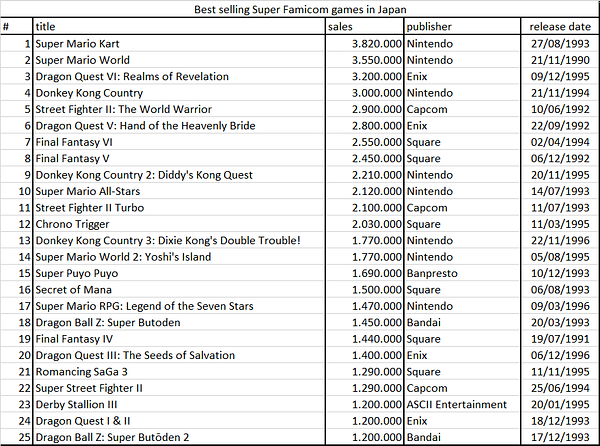

And finally for this week, we’re all about sales numbers here at GameDiscoverCo. And it’s the 30th anniversary of the SNES / Super Famicom’s release in Japan. (Super Mario World is my favorite game of all time, by the way!) So what better to end with than the all-time top selling Super Famicom games?

[This newsletter is handcrafted by GameDiscoverCo, a new agency based around one simple issue: how do players find, buy and enjoy your premium PC or console game. You can now subscribe to GameDiscoverCo Plus to get access to exclusive newsletters, interactive daily rankings of every unreleased Steam game, and lots more besides!]